Germany is pouring €500 billion into crumbling roads, outdated hospitals, and a military it neglected for decades. It’s the biggest fiscal gamble in the country’s post-war history. But is it a genuine turning point, or the world’s most expensive accounting trick?

Europe’s Growth Engine Has Stalled

Germany was supposed to be untouchable. For three decades after reunification, it was the export champion, the fiscal hawk, the industrial powerhouse that kept Europe moving. Then something broke.

The numbers tell a story that would have seemed unthinkable just five years ago. Germany contracted 0.1% in 2023, then again by 0.5% in 2024, before managing a barely-there 0.2% recovery in 2025.Three consecutive years of contraction or near-zero growth — and the reasons are not hard to find. While other countries invested through the low-interest-rate era, Germany saved. The result is visible everywhere: bridges that are crumbling, a railway that is chronically late, broadband speeds that lag behind much of Europe. Decades of underinvestment have quietly hollowed out Europe’s largest economy and now the bill has arrived.

The country that once powered Europe is now its weakest major link. And Berlin has decided it’s time to do something dramatic about it.

Breaking a Decades-Old Rule

To understand why this moment matters, you need to know about the Schuldenbremse: Germany’s “debt brake.” Enshrined in the constitution since 2009, it strictly limited how much the government could borrow. It was a point of national pride for fiscal conservatives. Politicians bragged about it. It was also, many economists argued, slowly strangling public investment.

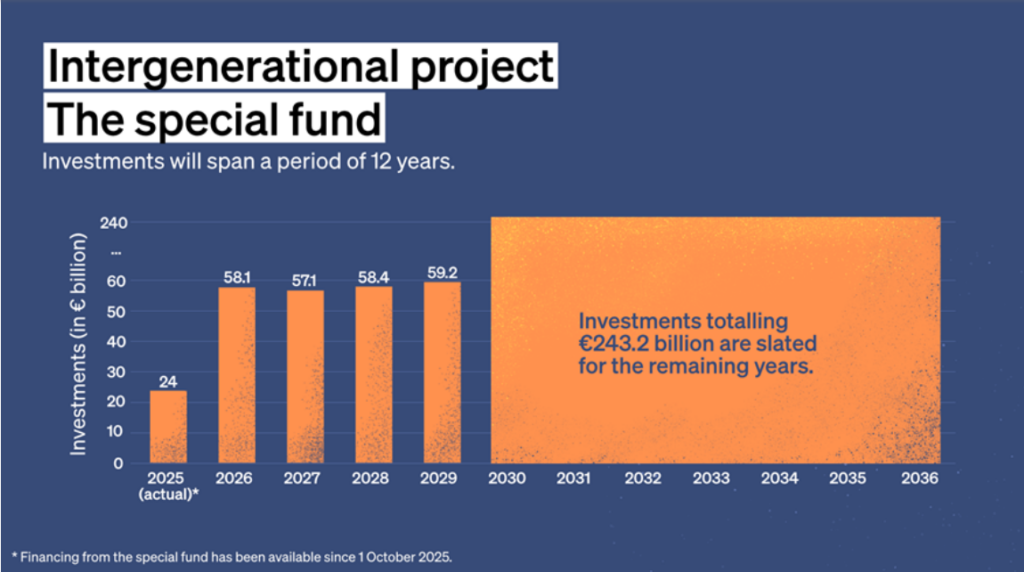

In March 2025, Chancellor Friedrich Merz’s government broke with that tradition decisively. German President Frank-Walter Steinmeier signed off on a landmark constitutional reform, effectively punching a massive hole in the debt brake and creating a €500 billion Special Fund for Infrastructure and Climate Neutrality, outside the normal budget constraints entirely. (Source: Herbert Smith Freehills Kramer)

The fund is structured to run for 12 years, split three ways:

- €300 billion for federal government investments

- €100 billion for climate neutrality targets by 2045

- €100 billion for regional and local infrastructure

(Source: German Federal Ministry of Finance)

It’s not just about filling potholes. It’s a statement that Germany is finally willing to borrow its way back to competitiveness.

Rearming at a Historic Pace

At the same time (and this is the part that would have been almost unimaginable a decade ago) Germany is rebuilding its military.

Germany’s 2026 defence budget stands at around €83 billion, up roughly 32% from 2025, making it the country’s largest military buildup in decades. (Source: Nordic Defence Review) By 2029, that figure is projected to more than double to over €152 billion, putting Germany on track to hit NATO’s target of 3.5% of GDP on defence spending before 2030. (Source: Clean Energy Wire)

The driver is no mystery. Russia’s war in Ukraine shattered decades of post-Cold War assumptions. American pressure on NATO allies to carry more of the burden, with the US pushing members toward 5% of GDP, has added urgency. Merz, in a notable February 2025 speech, warned it was “five minutes to midnight for Europe” and said the continent may need to achieve strategic independence from the US faster than expected. (Source: Reuters)

Combined with the infrastructure fund, this puts Germany’s total fiscal commitment at well over €1 trillion across the next several years. That’s a seismic shift for a country that used to make balanced budgets a point of national identity.

What the Money Is Actually Supposed to Build

So where does €500 billion go? The fund targets sectors that have suffered years of underinvestment:

- Transport: roads, bridges, railways

- Digital: broadband internet rollout

- Healthcare: hospital modernisation

- Energy: hydrogen infrastructure, EV charging, industrial decarbonisation

- Education: schools and childcare facilities

The need is real. Nearly 20% of German motorways and almost 30% of highways are already exceeding warning thresholds for surface condition, a tangible drag on an economy that depends on moving goods efficiently. (Source: Bitget News / institutional investor analysis)

The €100 billion climate component (a condition demanded by the Green Party in exchange for their crucial votes to pass the constitutional amendment) is channelled through the separate Climate and Transformation Fund, covering everything from energy-efficient building renovations to the hydrogen economy. (Source: Latham & Watkins)

The Reality Check: Is the Money Actually Landing?

Here’s where it gets uncomfortable and where this story becomes essential reading for anyone watching European markets.

A major Reuters-cited analysis published in March 2026 by two of Germany’s most respected economic institutes — the German Economic Institute (IW) and the ifo Institute — raised a serious alarm: much of the borrowing linked to the fund may not be generating genuinely new investment at all. Instead, economists argue, a large share of the money appears to be replacing spending that would have come from the regular federal budget anyway. (Source: European Times)

The Deutsche Bahn example is the clearest illustration. The fund earmarked €18.8 billion for Germany’s national railway in 2026. Simultaneously, the core budget’s contribution to the rail network shrank by €18.7 billion. Nearly identical figures. Similar patterns appeared in motorway bridge repairs, broadband rollout, and hospital support. (Source: Clean Energy Wire)

In a survey of nearly 180 senior economists by the ifo Institute, the verdict was sobering: on average, respondents estimated that only 47% of the debt-funded money would go toward genuine new investment. One in four economists put that figure at just 20%. (Source: ifo Institute)

The German government pushes back on this framing. The Finance Ministry argues the programme is legally additional: total federal investment spending rose from €74.5 billion in 2024 to €87 billion in 2025, with €120 billion planned for 2026. That’s real growth, they say, not a shell game.

Both sides have a point. The legal argument holds. But the political question is different: can Germany prove to voters, businesses, and European partners that this money is visibly changing the country’s foundations and not just moving numbers between columns?

What This Means for Markets

For investors and business leaders, this is the story to watch in Europe right now.

The structural thesis is intact. Germany needs this infrastructure, and the political will to fund it now exists. That part is genuinely new. But the near-term catalyst effect is being delayed by bureaucratic bottlenecks and slow disbursements. 2026 disbursement data is shaping up as the make-or-break signal: a clear acceleration in actual spending is needed to support growth forecasts and justify the optimism baked into European equity markets. (Source: Bitget News)

The ripple effects matter beyond Germany’s borders. As Europe’s largest economy, any genuine improvement in German growth spills outward: through purchases from non-German defence contractors, job creation, and stronger consumer and business spending across the bloc. (Source: Charles Schwab)

Sectors worth watching: transport and logistics, broadband infrastructure, defence industry, energy transition (especially hydrogen), and construction. The opportunity is real, but it will accrue to companies with the operational capacity to navigate Germany’s notoriously slow approval processes.

Bet or Bluff?

Germany has the money. It now has the political will, too. Something that seemed impossible even two years ago. The debt brake reform was historic. The scale of ambition is genuine.

But ambition and execution are two very different things. The criticism from leading economists is not a minor quibble, but a warning that announced billions mean nothing if they simply shuffle existing spending into a new column. Germany’s credibility as Europe’s economic anchor depends on whether the roads actually get built, the broadband actually gets laid, and the Bundeswehr actually gets modern.

The question was never really whether Germany could afford this bet. It was whether Germany could actually make it pay off.

That answer is still being written and the next 12 months will tell us a lot about which way it goes.